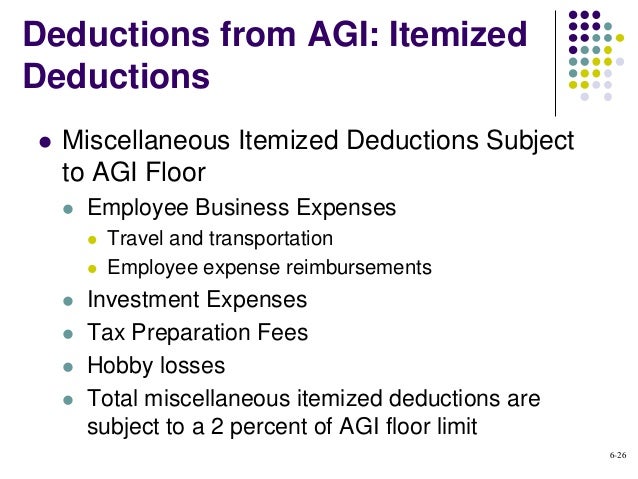

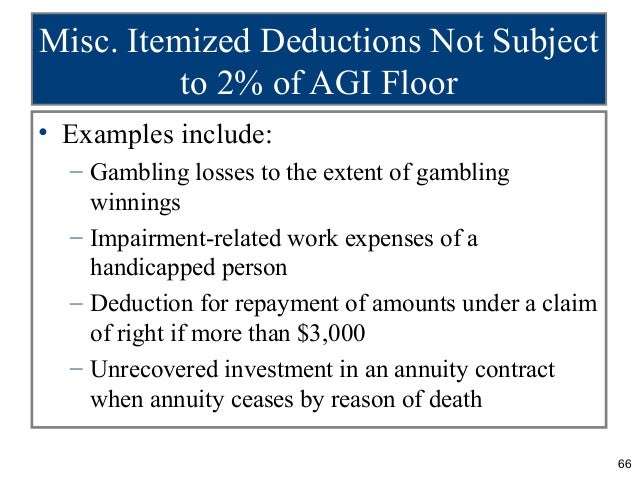

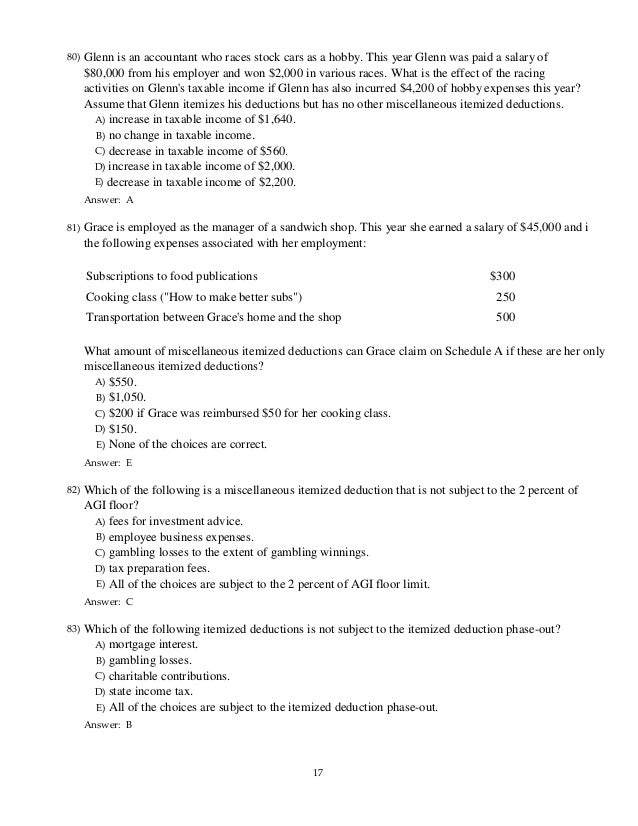

Miscellaneous Itemized Deduction Subject To A Two Percent Floor

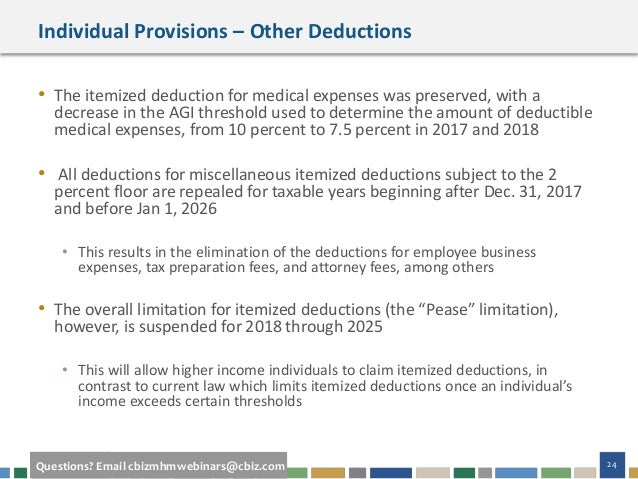

Tax Reform 2018 The Impact On Itemized Deductions For Individuals Jfs Wealth Advisors

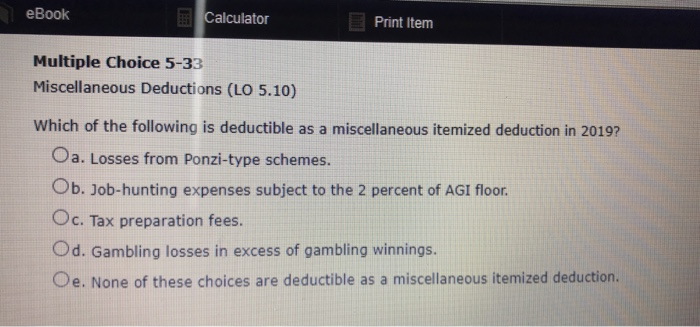

Solved Ebook Calculator Print Item Multiple Choice 5 33 M Chegg Com

Acct321 Chapter 06

Vol 01 Chapter 10 2015

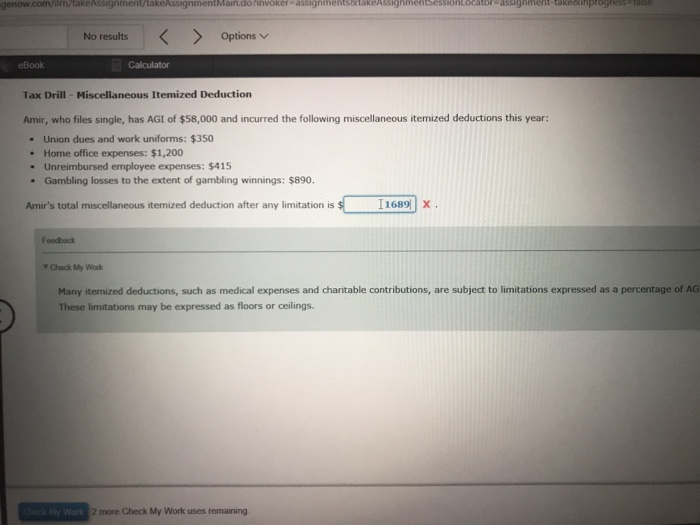

Solved I Need To Know How To Do This So Please Explain Yo Chegg Com

Taxation Of Individuals And Business Entities 2018 Edition 9th Editio

Unreimbursed employee business expenses such as.

Miscellaneous itemized deduction subject to a two percent floor.

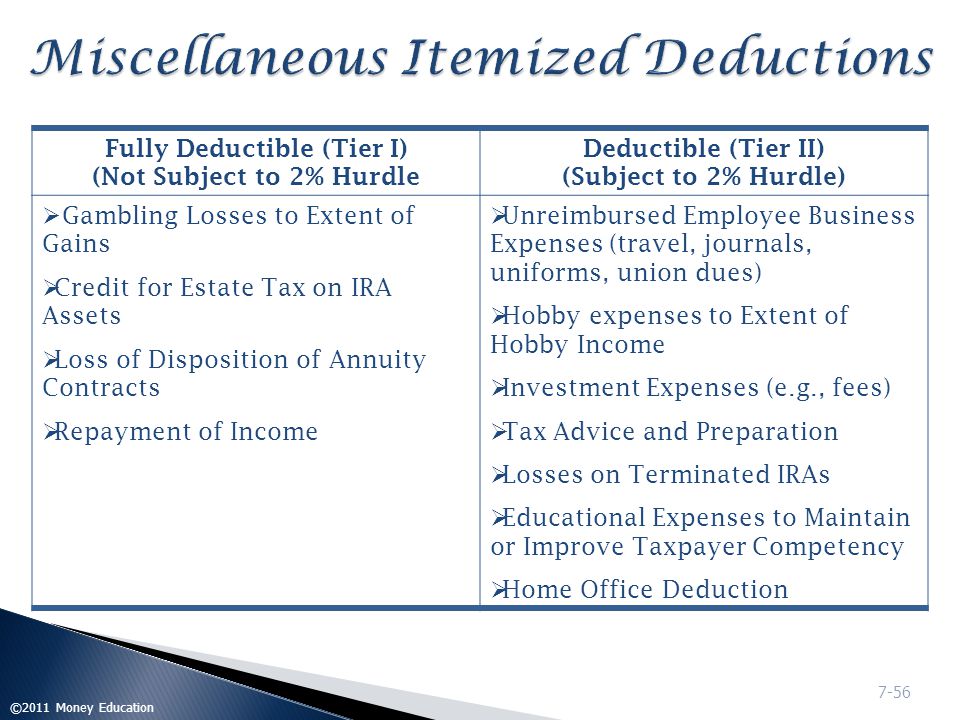

Itemized Deductions Chapter 7 C 2009 Money Education Ppt Download

Cfp Income Tax Planning Flashcards Quizlet

Webinar Slides Tax Reform S Impact On High Net Worth Individuals

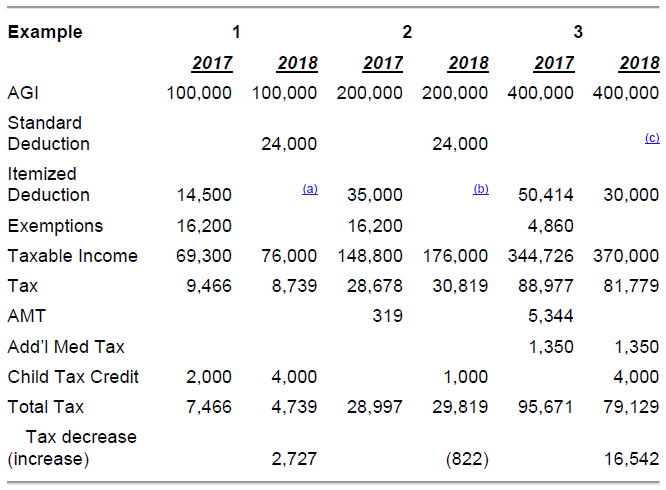

2017 Tax Cuts Jobs Act Impact On Families

Source : pinterest.com